![2024 Upgrade Tesla Model 3 Accessories Mud Flaps [Stay Clean, Protect Paint] All Weather…](https://techcratic.com/wp-content/uploads/2024/11/71zi71HyMhL._AC_SL1500_-360x180.jpg)

![CIA Whistleblower Sitting On Biggest UFO Secrets [Lue Elizondo Interview]](https://techcratic.com/wp-content/uploads/2024/11/1731796200_maxresdefault-360x180.jpg)

Dorothy Neufeld

2024-08-02 08:10:00

www.visualcapitalist.com

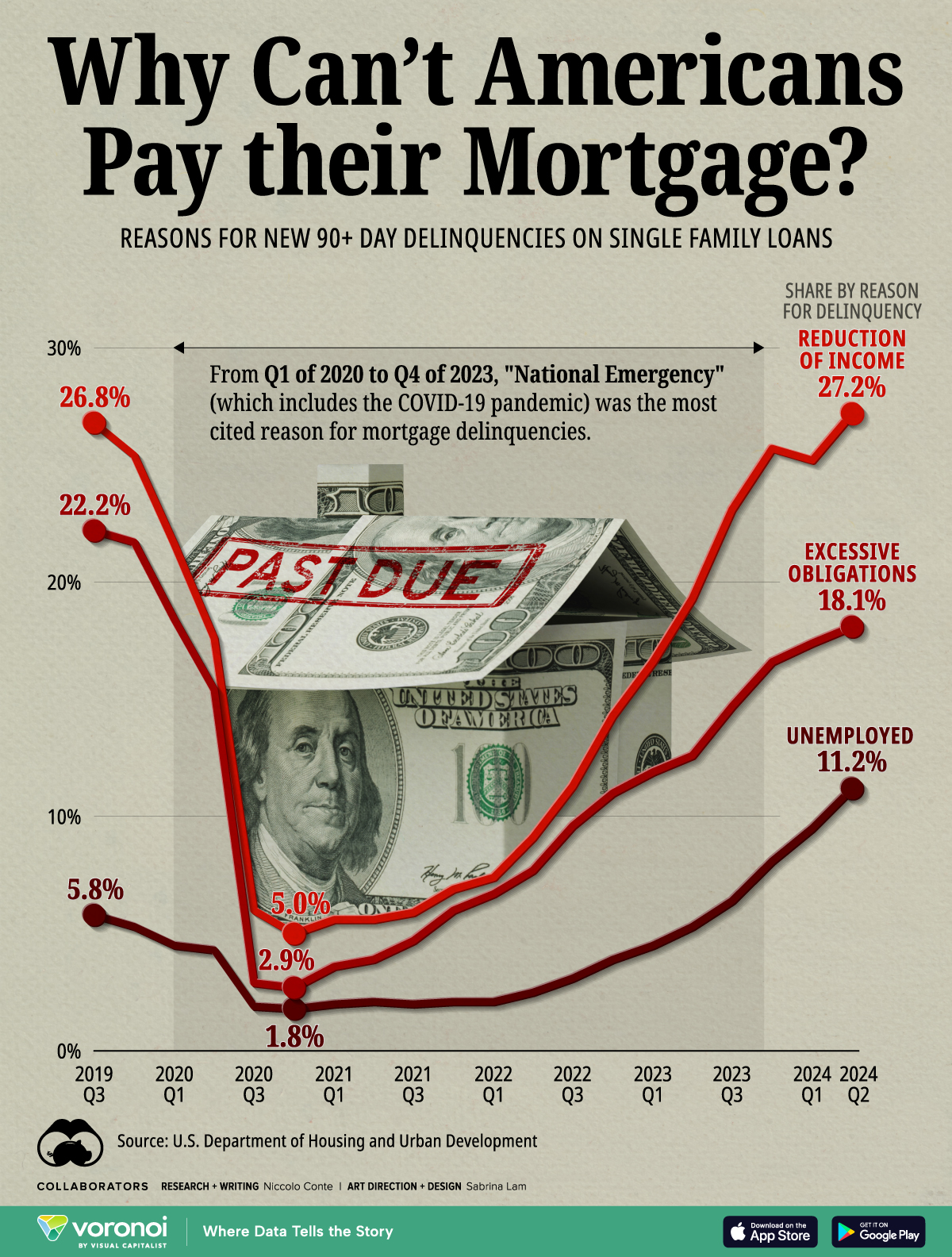

Why Can’t Americans Pay their Mortgage?

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

A rising cost of living is making it difficult for Americans to pay off their mortgage debt, or even purchase a home altogether.

Yet interestingly, mortgage delinquencies are at near-record lows. In the first quarter of 2024, the proportion of single-family residential mortgages in delinquency fell to 1.7%. By comparison, delinquencies spiked more than 11% during the global financial crisis. This resilience is partly due to homeowners locking in low rates before interest rates surged, sheltering them from the higher cost of paying off debt.

This graphic shows the financial reasons that Americans can’t pay their mortgage in 2024, based on data from the U.S. Department of Housing and Urban Development.

The Financial Reasons Driving Mortgage Delinquencies

Below, we show the financial reasons contributing to new mortgage delinquencies of 90 days or more on single-family homes:

| Fiscal Quarter | % Citing Reduction of Income | % Citing Unemployed | % Citing Excessive Obligations |

|---|---|---|---|

| 2024 Q2 | 27.2 | 11.2 | 18.1 |

| 2024 Q1 | 25.2 | 9.5 | 17.4 |

| 2023 Q4 | 25.7 | 8.1 | 16.6 |

| 2023 Q3 | 23.1 | 6.4 | 14.7 |

| 2023 Q2 | 19.3 | 5.3 | 12.6 |

| 2023 Q1 | 16.6 | 4.5 | 11.9 |

| 2022 Q4 | 14.3 | 3.9 | 11.0 |

| 2022 Q3 | 11.3 | 3.1 | 9.6 |

| 2022 Q2 | 9.1 | 2.5 | 7.7 |

| 2022 Q1 | 7.4 | 2.1 | 6.7 |

| 2021 Q4 | 6.9 | 2.1 | 6.0 |

| 2021 Q3 | 5.9 | 2.0 | 4.7 |

| 2021 Q2 | 5.6 | 2.1 | 3.9 |

| 2021 Q1 | 5.6 | 2.0 | 3.6 |

| 2020 Q4 | 5.0 | 1.8 | 2.7 |

| 2020 Q3 | 6.0 | 1.9 | 2.9 |

| 2020 Q2 | 17.6 | 4.3 | 15.4 |

| 2020 Q1 | 21.6 | 4.5 | 18.4 |

| 2019 Q4 | 25.4 | 5.3 | 21.7 |

| 2019 Q3 | 26.8 | 5.8 | 22.2 |

Despite a strong labor market, the share of Americans citing a “reduction of income” was the highest overall, sitting at pre-pandemic levels.

Often, cash-flow problems spurred by negative life events are the primary catalyst for mortgage delinquencies. A separate study shows that they were responsible for 70% of underwater mortgage defaults between 2008 and 2015, while strictly negative equity caused just 6% of these defaults. Underwater mortgages are defined as those where the principal owed on a home is worth more than the home value.

In many ways, this challenges the previously held belief that negative equity heavily triggered U.S. mortgage delinquencies during the global financial crisis.

Following next in line were excessive obligations, accounting for over 18% of responses in the second quarter of 2024. This figure has more than doubled over the last two years, at a time when credit card and auto loan delinquencies are at 10-year highs. In fact, Americans’ interest payments on non-mortgage debt now costs as much as mortgage interest payments for the first time ever.

Shielded from High Interest Rates

Looking ahead, the prospect of rising mortgage delinquencies remains uncertain.

Today, 96% of American homeowners have fixed mortgage rates, which often extend through the life of the loan. Many of these are more than 10 years, meaning that higher mortgage costs may not be a primary driver of bad loans for some time. Instead, rising unemployment or an economic downturn could have a more immediate and substantial impact on American homeowners in the future.

The post Why Can’t Americans Pay their Mortgage? appeared first on Visual Capitalist.

Support Techcratic

If you find value in our blend of original insights (Techcratic articles and Techs Got To Eat), our up-to-date daily curated articles from top technical news sites, and the extensive technical work required to keep everything running smoothly, consider supporting Techcratic with Bitcoin. Your support helps me, as a solo operator, continue delivering high-quality content while managing all the technical aspects, from server maintenance to future updates and improvements. I am committed to continually enhancing the site and staying at the forefront of trends to provide the best possible experience. Your generosity and commitment are deeply appreciated. Thank you!

Bitcoin Address:

bc1qlszw7elx2qahjwvaryh0tkgg8y68enw30gpvge

Please verify this address before sending any funds to ensure your donation is directed correctly.

Bitcoin QR Code

Your support is crucial for me to continue delivering valuable content and managing the technical aspects of the Techcratic news site. By scanning the QR code below, you help me keep providing insightful articles and maintaining the essential server infrastructure. Your generosity is greatly appreciated and allows me to sustain and enhance my work.

Privacy and Security Disclaimer

- No Personal Information Collected: We do not collect any personal information or transaction details when you make a donation via Bitcoin. The Bitcoin address provided is used solely for receiving donations.

- Data Privacy: We do not store or process any personal data related to your Bitcoin transactions. All transactions are processed directly through the Bitcoin network, ensuring your privacy.

- Security Measures: We utilize industry-standard security practices to protect our Bitcoin address and ensure that your donations are received securely. However, we encourage you to exercise caution and verify the address before sending funds.

- Contact Us: If you have any concerns or questions about our donation process, please contact us via the Techcratic Contact form. We are here to assist you.

Disclaimer: As an Amazon Associate, Techcratic may earn from qualifying purchases.